International diversification with the Motilal Oswal S&P 500 Index Fund

Issue #11

Over the past couple of years, there’s been some increasing chatter among Indian investors if they should diversify internationally. I’ve received numerous queries on Twitter. The opportunity costs and the associated trade-offs of home country bias - the tendency of investors to invest only in their home countries have been well documented in the academic literature. It intuitively makes sense to diversify globally, but it’s very hard to do so India. We have a bunch of feeder funds, but the problem is that they are costly and in some cases, just sub-par choices and I’ve personally never been a fan of these funds. It makes absolutely no sense to invest in feeder funds which invest in costly active funds when there’s overwhelming evidence of the inability of the underlying funds to even match the performance of broad benchmarks, let alone beat them.

Indian investors can rejoice in the fact that Motilal Oswal is finally launching an S&P 500 index fund.

People had been asking my view on this fund on Twitter and just when I was wondering if I should write something, Avinash graciously reached out and offered to write a piece for us. Now, I’ll just take a minute to reiterate what I’ve said earlier. I had no idea that this newsletter would grow enough for other people to write on it and I’m super psyched about all the comments we’ve been getting about how the newsletter has helped investors - that was the goal. So, I’d like to express my gratitude to you, the reader and also Avinash for writing for us for the second time. Sorry for the longwinded intro and read on…

Avinash Luthria is Founder, SEBI Registered Investment Adviser (RIA)&Fee-Only (Advice-Only) Financial Planner at Fiduciaries. He was previously a Private Equity & Venture Capital investor for 12 years and has a flagship-course MBA in Finance from IIM Bangalore; He writes about Financial Planning & Investing in Business Standard, Mint, The Ken, MoneyControl, FreeFinCal, VCCircle etc. This article is not Investment Advice and is not a Research Report. Views expressed here are of the author and do not necessarily reflect the views of the Indexheads newsletter.

Finally, a way to invest abroad with the Motilal Oswal S&P 500 Index Fund

COVID-19 makes almost everything else seem irrelevant. And it feels irrational to focus on any other topic. Further, it feels almost immoral to be doing anything unrelated to mitigating the COVID-19 disaster, particularly for people that we know personally and more so for the sub-set that is less well off. So, I felt extreme revulsion at the thought of writing this article. But not writing this article would be escaping from what I am uniquely qualified to do, which is why I felt compelled to do it. These are a few (but not all) of the reasons why I finally decided to write this article:

A year-and-a-half back, I wrote an article in Business Standard called ‘You can mitigate domestic risks by investing abroad - Open a low-cost international broking account and invest in low-cost international exchange-traded funds’ and these are a few very mildly edited excerpts with a few parts highlighted:

Neither domestic equity nor domestic real estate can be relied upon to mitigate several country-specific tail risks. Noted financial theorist William J Bernstein categorised such deep risks as [hyper] inflation, confiscation, devastation and deflation. Inflation includes very high inflation or hyperinflation, as seen in Argentina and Brazil around 1989. Confiscation could be overt or covert. Overt confiscation becomes more likely as a country becomes less democratic, while covert confiscation includes very high tax rates. Devastation is primarily caused by war, including a major terrorist attack [and as we understand in 2020, by a pandemic]. And finally, there is deflation, the rarest category of risk, as witnessed in Japan in 1989 and Greece in 2013. Such tail risks are too rare to attach probabilities to, but they are nevertheless relevant…

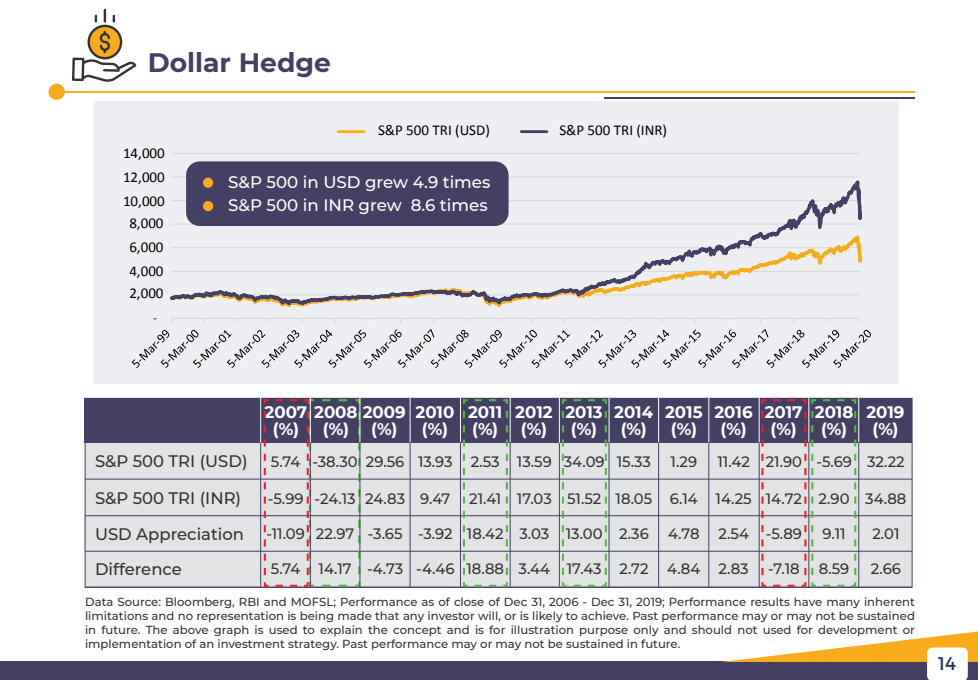

International investments, including equities, offer better, though not complete, mitigation against some of these country-specific tail risks. The primary reason one should invest in international equities is to diversify one’s risk by not putting 100 per cent of one’s net worth in one country, India, which contributes just 3.3% of world nominal GDP [and makes up just 1.1% of the Vanguard Total World Stock Index Fund]. None of us would be willing to put 100 per cent of our net worth in Italy, which is an economy of a comparable size. This is despite Italy’s S&P sovereign credit rating being one notch higher than India’s. India’s credit rating incidentally is one notch above junk…

Since India’s mutual fund industry is still maturing, ideal options [to invest outside of India] don’t exist. However, a hypothetical ideal option provides a baseline to compare the actual options against. The hypothetical ideal option is an Indian low-cost feeder fund that invests in the Vanguard US S&P 500 ETF, or the equivalent index fund.

I first started pushing for such a product more than 10 years back. As a part of my job at that time, I was in discussions to become a Private Equity majority shareholder in Benchmark Mutual Fund (though the founders would continue to be significant shareholders and run the company; the postscript to this article elaborates a bit. Benchmark Mutual Fund was the only mutual fund (MF) in Indian mutual fund history to be focused on index funds, and it did this mainly through an ETF structure. The feedback then was that there was no demand for this product among Indian investors.

I re-started pushing for such a product a couple of years back when I became a SEBI registered Investment Adviser and a Fee-Only (Advice-Only) Financial Planner. The feedback continued to be that there was no demand for this product among Indian investors. Motilal Oswal MF was the only MF house that themselves was interested in such a product. So, I had many meetings and discussions with them about this, including with many different people at Motilal Oswal MF. Naturally, the MF houses have a better understanding of various marketing constraints and the resultant cost constraints than what I have. This helped me to understand why the product structure had to be marginally different from what I had described in that article in Business Standard. It was understandable that an Indian MF would prefer a structure of the scheme directly holding the underlying US shares (instead of being a feeder fund/scheme to a Vanguard US index fund). Accordingly, the Indian scheme would have to pay material fees to S&P (the provider of the S&P500index) and that would increase the fees of the scheme.

But there were several other important nuances that I continued to have a strong view about. Accordingly, I kept requesting for the product to be an Indian index fund structure which invests in the US S&P 500 index (i.e. the US shares). I strongly preferred that structure to (a) an Indian ETF structure which invests in the US S&P 500 index and (b) an Indian Fund-of-Fund structure which invests in an Indian ETF structure which invests in the US S&P 500 index. This is a complex technical topic, so I won’t go into the details. My rationale is that the Indian index fund structure, which invests in the US S&P 500 index is the ideal structure for Indian retail investors and Indian HNI investors. On the other hand, the Indian ETF structure which invests in the US S&P 500 index would not be actively traded and hence was relevant primarily for Indian Ultra HNI investors. (Note: To clarify, I like the Nippon India Nifty 50 ETF which is actively traded. So, this preference for a particular structure in this particular context is a nuanced point and is not a generic preference for or against the ETF structure.)

Since Motilal Oswal MF is launching a product that I was pushing for and with exactly the structure I was requesting for, I felt that I have a duty/obligation to write about it (Note: Naturally I was one voice out of a large number of voices that Motilal Oswal MF considered while making their decision. So, I do not mean to imply that I had a material role to play in their decision). There is only so much that I can personally do to mitigate the COVID-19 disaster for human beings, particularly for people whom I personally know and more so that are less well off. Not doing the one unrelated and far less important thing that I am uniquely qualified to do (write this article) felt like being an escapist.

Bad Indian MF products get high (retail) Assets Under Management (AUM) and good MF products get low (retail) AUMs (you could compare the AUM of the very good Nippon India Nifty 50 ETF vs. the AUM of various nonsensical sector-specific funds such as ‘Power & Infra Fund’). The rule with Indian MF products almost seems to be ‘no good deed will go unpunished, and no bad deed will go unrewarded by Indian investors’. This article is my tiny contribution to fixing this distribution of (retail) AUM between MF products and encouraging good MF products. I also have a convoluted hope that maybe this article helps some readers to be marginally more financially secure and then that might make it (psychologically) easier for them to be more helpful to their relatives, friends, employees, including those who are less well off.

However, since I currently have almost zero mental bandwidth for anything other than COVID-19, I am writing this article in almost one sitting, with zero incremental research, almost-zero fact-checking and this led to the FAQ format. The information in this article is not exhaustive and is on a best effort basis at the time of writing this article. Also, I do not accept any responsibility for errors/omissions. Further, this article is not Investment Advice, and it is not a Research Report. Finally, I obviously do not get any payment from any product manufacturer (e.g. Motilal Oswal MF) for writing this article.

These FAQ’s are targeted at someone who is already interested in such a product and hence does not aim to convince anyone about such a product:

1. What is the product?

The Motilal Oswal S&P 500 Index Fund (MOFSP500) is an Indian index fund structure that invests in the US S&P 500 index. You can find additional information about the product in the Scheme Information Document (SID).

Note: Please do not confuse this with the ‘Motilal Oswal Nifty 500 Fund’ which invests in the Indian Nifty 500 index).

This article ignores a very large number of aspects that are covered in the SID since that is available for the reader to read for themselves, e.g. there is an exit load of 1% if an investor exits on or before 3 months from the date of allotment.

2. What are the fees?

For simplicity, let’s focus only on the Total Expense Ratio (TER) though there are other typically smaller costs/fees (for simplicity, this article uses the terms fees and TER interchangeably). The precise TER will be known only a few days after the New Fund Offering (NFO) period which is currently scheduled for 15th to 23rd April 2020. I am making an educated guess that the TER for the Direct Plan will be approximately 0.5% per annum; p.a. (Note: This educated guess could be wrong; What we know from the SID is that the TER for the Regular Plan / Commission Plan will be less than or equal to approximately 1% p.a.)

The final TER will be known a few days after the NFO period ends. So, if you would prefer to know the final TER before you decide whether to invest or not, you could wait for a few days after the NFO period ends.

The fees are much higher than for the Indian Nifty 50 Index fund / ETF but the more relevant comparison is to other existing comparable products in India.

3. Do you prefer this product to the existing comparable products in India?

For the sake of brevity, I will compare the Motilal Oswal S&P 500 Index Fund to the most relevant/comparable option for retail and HNI investors, which is the Franklin India Feeder Franklin US Opportunities Fund. The Franklin India Feeder Franklin US Opportunities Fund Direct Plan has total fees in the ballpark of 1.4% per annum (the total fees are the fees at the India level as well as at the US level). The Franklin India Feeder Franklin US Opportunities Fund invests in the Franklin US Opportunities Fund which is an active fund and it is natural that it will have higher fees than an index fund. But since US active funds on the average significantly underperform the relevant index, I prefer fees of 0.5% p.a. for an index fund to fees of 1.4% p.a. for an active fund.

There are pros and cons for each product, so my preference is naturally subjective i.e. not objective. In summary, I prefer the Motilal Oswal S&P 500 Index Fund to all other Indian mutual funds which allow you to invest outside of India.

4. Do you prefer this product to investing in the Vanguard US S&P 500 ETF through a foreign broking account?

This is a complex topic and hence it is outside the scope of this article. A few of the simpler aspects(i.e. not the complex aspects) are covered in the Business Standard article mentioned earlier and mildly edited excerpts are copy-pasted here with a few bits highlighted:

To avail of this [option i.e. the Vanguard US S&P 500 ETF], one needs to first open a low-cost foreign broking account directly from India [e.g. with Interactive Brokers]. Such a broking account’s cost (minimum guaranteed revenue for the broker) of $10 per month subjectively makes it ideal for someone who expects to have a cumulative investment of at least Rs 5 million through this route, over the next five years. The second step is to transfer funds from India into the broking account in the US under India’s Liberalised Remittance Scheme (LRS). The final step is to stagger the purchase of the Vanguard US S&P 500 ETF over several years.

This route has three important tax-related disadvantages. One, your Indian income tax returns will become more complicated because you will be forced to separately disclose all foreign assets and income. Two, India’s ambiguous tax laws force one to assume that US ETFs will be taxed like US equity shares. Accordingly, if one holds such US ETFs for more than 24 months, then after indexation benefit one will have to pay capital gains tax at a rate of around 20 per cent. Three, while this route currently does not objectively increase the risk of a tax scrutiny, these rules could change in the future. Such a tax scrutiny would distract the investor from his job or business. Hence, an investor thinking of taking this route should consult a chartered accountant about all these three taxation-related aspects…

If you use one of the feeder funds available in India that invest in US equities[or the Motilal Oswal S&P 500 Index Fund], you will enjoy a few advantages. Your tax filing will not become more complex. You will also enjoy clarity that your investment in this fund will be taxed like a debt mutual fund. It will also eliminate [more precise language would be ‘not increase’] any possible future risk of tax scrutiny.

5. Doesn’t an investment in such international equity funds being taxed like a Debt MF bother you (compared to Indian equity MF taxation)?

This is not a detailed discussion of the taxation aspects. This is merely a high-level summary which ignores various details and nuances and some of them could be important to you (e.g. the so-called Super-Rich tax). So please consult your CA about any taxation related aspects. Taxation for MFs is calculated for each tranche (something like for each unit) but for simplicity, this section of the article assumes that you make only one investment ever. Also, the description here applies to any other such International Equity MF.

Motilal Oswal S&P 500 Index Fund is in substance an International Equity MF. But purely for the sake of taxation, an investment in the Motilal Oswal S&P 500 Index Fund is taxed like a Debt MF. Hence if you (an individual) stay invested for less than 3 years, then the gain is taxed at the income tax rate plus Surcharge (including Super-Rich tax) plus Cess. And if you stay invested for more than 3 years, then the gain net of indexation benefit is taxed at the Long-Term Capital Gains tax rate of 20% plus Surcharge (including Super-Rich tax) plus Cess.

As a comparison, an investor who invests in an Equity MF such as the Indian Nifty 50 Index Fund / ETF and stays invested for more than 1 year does not get any indexation benefit but pays a lower Long Term Capital Gains tax rate of 10% plus Surcharge (but not Super-Rich tax) plus Cess.

I am focused on the investor who will most likely stay invested for more than 3 years. Further, for simplicity let’s focus on an investor who will not have to pay Super-Rich tax at the time of exit (which could be during retirement). For such an investor, it is not clear whether the Equity MF tax structure is better, or the Debt MF tax structure is better. Oversimplifying a bit, they are both roughly equally good (or bad).

6. How much can one invest in such a product?

The Vanguard Total World Stock Index Fund provides a very rough theoretical/conceptual starting point to figure out what an individual’s equity portfolio could look like (to clarify, it does not provide a direct answer). And the Vanguard Total World Stock Index Fund consists of 1.1% of Indian equity and 55.8% of US equity (with the rest being other countries). For an investor anywhere in the world, the onus of proof is on anyone who argues against this country-wise sub-allocation (for brevity, I am leaving out the topic of country-wise sub-allocation in fixed income investments). Subjectively and theoretically, there is a strong argument that for a resident Indian, one’s equity allocation should be almost entirely to international equity (for brevity, this article will not go into this theoretical point). But practically, this is quite difficult to do (even if it is not impossible to do). The primary practical constraint for me personally is that I like to limit my investment via each MF house (e.g. all schemes of Motilal Oswal MF put together or all schemes of HDFC MF put together) to not more than 10% of my total net worth (i.e. total assets including primary residence if any minus total liabilities). Further, there are insufficient attractive products and different fund houses for resident Indians to invest in international equity. So, combining these two constraints, it makes it quite difficult to invest a signification portion of one’s net worth in international equity (but it is not impossible to do so).

Let’s consider an illustration of a resident Indian. To reiterate, this is just a hypothetical illustration, and this is not Investment Advice. Let’s say that Mr. X would like to allocate 40% of net worth to equity. Then the question of whether Mr. X should allocate 30% of net worth to international equity or 40% of net worth to international equity becomes a less important question today. As explained earlier, there are insufficient attractive products and different fund houses. So practically, it is quite difficult to invest 40% of net worth in international equity (but it is not impossible to do so). Let’s say that due to these reasons, Mr. X is forced to limit international equity to 15% of net worth. Then X may decide to allocate 10% of net worth to the Motilal Oswal S&P 500 Index Fund and 5% of net worth to some other international equity product (not via Motilal Oswal MF). Further Mr. X may decide to stagger the total investment over time (i.e. during the NFO and after the NFO and possibly even over a long period of time). Finally, Mr. X may decide to first redeem an existing equity MF investment and once those proceeds are available in Mr. X’s bank account, only then to invest in the Motilal Oswal S&P 500 Index Fund.

To clarify, the Liberalized Remittance Scheme annual cap for an individual does not place any cap on the quantum that an individual can invest in products such as the Motilal Oswal S&P 500 Index Fund.

7. Is it necessary to invest during the NFO?

No. If one decides to invest in this product, one could invest during the NFO, after the NFO or both. Further, one could also decide to stagger one’s investments over time (including via a SIP).

8. How can one invest during the NFO?

You can pretty much invest on any of the mutual fund platforms that you are investing through currently. Or one could invest via the Motilal Oswal MF website.

9. What key questions (related to this product) have you left out of this article?

Some of the relatively less relevant and / or irrelevant questions that I have left out of this article are:

“My expenses are mainly in Rupees and not in Dollars, so is such a product relevant to me?”

“What about exchange-rate-risk?”

“Does this mean that you prefer to invest in the US equity rather than in Indian equity?”

“Is this a good time to invest in equity and / or US equity?”

10. What key relevant questions (related to this product) have you left out of this article?

These are a couple of questions that I have left out for the sake of brevity and also because the answer varies significantly from person to person:

“Most MFs have Relationship Managers (RM) for Direct Plan investors. And some MFs get their RMs to contact Direct Plan investors to push expensive products (with high fees) such as Active MFs and also usually very expensive products such as PMS and AIFs. So, investing with an additional MF house potentially increase one’s risk of being sold a (very) expensive product. So, the relevant question becomes the net effect of the positive aspects of a useful product and the negative aspects of the risk of being pushed to buy a (very) expensive product. Is that net effect positive or negative?”(Note: The more knowledgeable the investor, the lower is this particular risk. And I have previously written half-a-dozen articles saying that one should follow a ‘buyer-beware’ approach in deciding whether or not to buy a product from an MF house or Asset Management Company. So, I am won’t repeating those points over here.)

“Due to COVID-19, does it make sense for me to spend even a minute of my time on medium-term/long-term action items such as this product?”

A few other relevant articles by Avinash Luthria:

The delusion of alpha

Second order thinking explains why you should invest in index funds and also the most suitable index fund products-- All your domestic MF investment should be in index funds and index-like funds with fees of less than 0.20% p.a.

The average Indian Active Mutual Fund does not beat the index

Ignore false arguments against index funds.

Reading the S&P Index Versus Active Funds India report will change the way you invest

Indian mutual funds, as a whole, do not beat the index()

Turn no-free-lunch from an opponent to an ally

Don’t waste your energy fighting the law of no-free-lunch. Instead use it as a tool for thinking, to avoid mistakes and also minimize costs through index funds.

Why it’s a myth to say that equity is safe in long term

Often, people take too much risk believing the myth that equity is safe in the long term

How much money do you need to retire?

This simple formula provides the answer

Myths about Indian vs US equity returns, rebalancing, back-testing, interest-rate-risk etc A lot of propaganda in personal finance contradicts the fundamental law that there are no free lunches

Podcast: The Boglehead Approach to Investing in India

Almost everything you have heard about financial planning and investing is wrong

Very informative article 👍

Good Insights 👍