Is my beta smarter than yours?

Issue #4

“Smart Beta makes me sick”

William Sharpe, Nobel laureate

The origins of the term “Smart Beta” are not very clear. Value and small-cap investing styles have been used by active managers for long now. In the last couple of decades, after Fama and French’s seminal 1992 paper, “The Cross-Section of Expected Stock Returns”, index providers realized that these styles could be delivered to investors in transparent rules-based indexes.

Let us get some definitions in place to set the context here before we dig into betas – smart and dumb.

What is a Factor?

Factor is a numerical characteristic or set of characteristics common across a broad set of securities e.g. cheap valuation, small size of company, high ROE and profitability, high returns over a lookback period, less volatile than other stocks, etc.

For e.g. Warren Buffett’s portfolio was deconstructed, to identify the source of his returns over the years, in a very insightful paper called “Buffett Alpha” by AQR. It does an excellent job of deconstructing the sources of his returns. Buffett bought stocks that were safe, cheap, high quality and large. The most interesting finding in the study was that stocks with these characteristics tend to perform well in general, not just the stocks with these characteristics that Buffett buys.

It turns out that Buffett owes his success to his identification of key common characteristics and not due to his stock-picking skills. However, Buffet’s genius lies in identifying these features, decades before modern financial theory caught up with him and his temperament because of which he stuck to his process for over 4 decades now.

What is Beta?

Beta is simply the exposure of a stock, mutual fund or portfolio to a Factor as defined above. The most common one being Market Beta which is generally referred to as only “Beta”. Contrary to popular perception, market beta is not the same as volatility, although it is closely related. Market Beta is the degree to which an asset tends to move with the broader market. So, to get exposure to market beta one would own a "market portfolio" or a portfolio of all the stocks in the market to get a market beta of 1 or complete exposure to the factor.

What is factor-based investing?

Continuing with the same example as above, if we were to apply a numerical definition to filter quality stocks (e.g. ROE > 15%, Leverage less than 2, Profitability > 10%) and built a diversified portfolio of these stocks we would investing in the Quality Factor. We would assess this portfolio regularly, say on a 6 monthly or yearly basis. We would drop those companies that no longer meet our criteria and continue to hold those that do. We would replace the companies that we have sold with new companies that now meet our criteria. This is simple words is rebalancing or “keeping winners and cutting losers.”

Many of the anomalies that factor investing exploits, derive their existence from human behavior, which is why they are not arbitraged away over time.

The simplest form of factor investing would be buying a low-cost passive broad-based index fund like the Nifty 50 in India and the S&P 500 in the US. Nifty 50 ETF has a long enough history in India and it is a single factor fund – you get only Market Beta, which by the way is good enough to beat 90% of fund managers.

There have been other multi-factor funds like (Reliance) Nippon Quant Fund which was launched in 2008 and is still being run. It claims to run a proprietary system based on factors like earnings, price momentum, quality. But we don’t how each factor is weighted in the model. Recently an institutional backed PMS has also launched an offering based on two factors – Momentum and Low Volatility. But it is early days. Indian Fund managers are yet to come up with an offering that is fully systematic, purely quantitative and true to label.

In a recent book, “The Man Who Solved The Market: How Jim Simons Launched The Quant Revolution” by Gregory Zuckerman, there is an interesting anecdote about Bob Mercer (The co-creator of IBM Watson and CEO of Renaissance Tech after Simons retired).

Source: Wikipedia

{kind=link}

Mercer was once in a meeting with the representatives of a West Coast endowment. Asked how the firm made so much money, Mercer offered an explanation. “So we have a signal, Sometimes it tells us to buy Chrysler, sometimes it tells us to sell.” There was pin-drop silence in the room. Chrysler hadn’t existed as a company since being acquired by Daimler back in 1998. Mercer hadn’t noticed. He was a quant, so he didn’t actually pay attention to the companies he traded.

He only looked for some common set of numerical/quantitative characteristics in stock price data. The names didn’t matter to him. If you are wondering, whether the endowment went ahead with their investment, then hell yeah, they did. RenTech was having trouble keeping investors away and still does till date. When Indian fund managers reach this state, then we can say that they are true systematic and quantitative in their investing approach.

Factor Zoo

In 2011, in his presidential address to the American Finance Association, John Cochrane of the University of Chicago coined the term, "Zoo of Factors". The paper (....And the Cross-Section of Expected Returns, 2015)" reported that 59 new factors were discovered between 2010 and 2012 alone. In total, they studied 315 unique factors from top journals and well-regarded working papers. But not all these factors were actually unique or investible.

What are the characteristics of investable factors and which are the ones that pass the test?

Authors Larry Swedroe and Andrew Berkin in their book "Your Guide to Factor-Based Investing" state that for a factor to be worthy of investment it must pass the following tests". They must be

1. Persistent - Hold across long time periods and market regimes

2. Pervasive - Hold across geographies, sectors and even asset classes

3. Robust - Hold for various definitions (for eg there is a value premium whether measured by P/B , earnings, cash-flow or sales)

4. Investable - It should actually be implementable after trading costs

5. Intuitive - Should be backed by logical risk or behavioral based explanations for its premium and why it should continue to exist.

Which are the factors that make the cut?

1. Market Factor - The tendency of riskier equity as an asset class to outperform a risk free bond over the long run.

2. Value – The tendency for relative cheap assets to outperform relatively expensive ones. Also known as HML or High Minus Low i.e. High Book/Price Stocks (cheap) minus Low Book/Price Stocks (expensive)

3. Size Factor – Degree to which a returns of small cap portfolio beat returns of a large cap portfolio. All known as SMB or Small Minus Big.

4. Momentum -Tendency for assets that have performed well (poorly) in the recent past to continue to perform well (poorly) in the future, for a period of time.

5. Low Volatility – Tendency of stocks with low volatility to deliver both higher absolute and risk adjusted returns than most high volatility stocks.

6. Quality – tendency of firms with high profitability measured by earnings have high subsequent returns after controlling for value factor as measured above.

Quality and Investment are two recent factors that Fama and French have added to their 3-factor model, which is now a 5-factor model. Still no momentum or low volatility in their world. Mark Carhart, in his study “Ön Persistence in Mutual Fund Performance” was the first to use momentum together with the three Fama-French factors (market beta, size, and value). The data below should be enough to tell you that Momentum is empirically the most robust factor out there. Both in absolute terms as well in terms of risk-adjusted returns.[1]

Source: Your Guide to Factor-Based Investing

There are risk-based and behavioral explanations for market, size and value factors. Momentum and Low Volatility have better behavioral explanations than risk-based ones. But have equally good if not better empirical evidence that they indeed work. However, they go against conventional finance theory, particularly EMH and CAPM. And we don’t want to interfere with that, do we? However, it should be telling that WEB, Soros, or Simons, don’t believe in the absolute version of EMH i.e. markets are perfectly efficient. Markets are not perfectly efficient, but they are, however, efficient at most times. And they are tough but not impossible to beat.

“It’s a high-pressure world. And when your factor is not working, it’s not an easy time,” Cliff Asness says. “But if we can’t keep emotion out of our own brains, it’s pretty good news for the factors, for the idea that investors aren’t perfectly rational is the reason these factors work.”

Are other betas really “smart”er than market beta?

Smart Beta in my view is merely a marketing term to distinguish other factors/beta from “Market Beta” which has been around the longest and is the underpinning of Passive Index Investing.

Smart Beta is a term used for other factors like size, quality, momentum, etc. or if the portfolio of stocks in say a Market Beta fund is constructed with different weights. It’s like saying if we played with a heavier bat like Sachin Tendulkar, we would have more power in our shots, or if we changed the weight of our bats depending on where we are in the stage of the game like Dhoni does, then we will have an edge over the bowler.

Ultimately all bats will make runs if the cricketer stays at the crease and connects. Some bats are heavier and some are lighter. Sachin’s bats are not “smarter” than Dhoni’s. Smart is not an attribute we can apply to betas too. They all have different sources, but ultimately they are there to deliver returns to you.

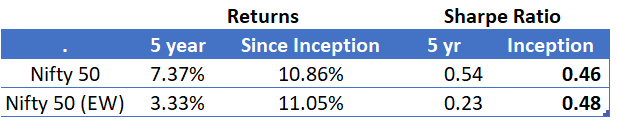

Now the most popular and simple form of getting exposure to market beta is buying a fund replicating a market cap-weighted index. However, some believe that an equal cap-weighted index is better. And it is sold as a “smart market beta” index fund.

How is it smarter? It certainly hasn’t been smarter in the last 5 years. And even since inception isn’t significantly different. The difference is about 19 bps. If you fell for the smart beta marketing shenanigans and paid over 19 bps more in fees for an equal weighted Nifty 50 fund, you had a bad five years and no enhancement in expected returns.

Let us look at the other Betas or Factors, other than Market Beta. Fama is reported to have said, that any additional expected return from smart beta is a result of assuming a higher risk. However, Fama, speaks with a forked tongue on this. He is only partially correct. The data does not support him here. While some factors do not beat market beta factor on a risk-adjusted basis, some like momentum and low volatility beat it hands down. Ironically the factors that Fama includes in his model are the ones that underperform market beta on a risk-adjusted and absolute basis.

Data shows, Market Beta has a Sharpe ratio of 0.40 and is above Size and Value on an absolute and risk-adjusted basis. But Momentum beats all of them on an absolute and risk-adjusted basis with a Sharpe ratio of 0.61. But in Fama’s world, Momentum is a premier anomaly and not a factor. Ok Boomer. Aswath Damodaran, Professor of Finance at the Stern School of Business at NYU, says “When Gene calls it an anomaly, what he means is we cannot explain it using fundamentals. It’s an anomaly –”

While Fama, was open-minded enough to let Asness, pursue his thesis if the data supported it, and has also grudgingly accepted "momentum" as a premier anomaly, he still refuses to put it his factor model, even after he has expanded his single factor model to a five-factor model now to include, value size, quality/profitability and investment (even though the last is not quite robust).

It works over time, but not all the time

As simple as factor investing may sound, it is far from easy. They work over time but they don’t work all the time. And when they don’t work, it is very tough to keep going and following your process. Like a batsman out of form, you may have to tweak your technique, but you can’t suddenly start batting left-handed if you are naturally right-handed. You just must survive the difficult patch, think through your process and not get thrown off your game. It’s a mind game at that level. Most things are. Skill takes you up to a point. After that, it’s your temperament and psyche.

These fancy theories are good for developed markets. They don’t work in India

Ok. Boss. good gyan. Now tell me does factor investing work in India. You know we are a developing country and our markets are inefficient, fund managers can still squeeze out enough alpha to earn their 2% fee. Seriously? Ok maybe in large-cap it’s getting tough for them. But in small and mid-cap they are can still outperform. Oh puhlease! The data doesn’t support this too. In Large Caps, it is worse than a coin flip. Even in Mid/Small caps over 1,3,5 years majority of Mid Cap funds failed to beat their benchmarks and over 10 years it’s just about a coin toss. And if you think your advisor has the clairvoyance to predict coin tosses, go for it. But only “explore” portion. If you must sin, sin a little.

Ok, maybe Market Beta works. But what about your other fancy factors Momentum, Value, Size, etc. - am sure they don’t work in India. So thankfully for me, the good folks at NSE have created indexes based on these factors and you don’t have to take my word on it.

Data says they do. Momentum (Alpha 50) and Low Volatility, in fact, work the best in India, as they do globally. Are they investible? While we do have an ETF by ICICI based on Nifty Low Vol 30 but nothing yet on other indexes. DSP has launched a quant fund which is a multifactor fund on quality, value, low volatility but the parameters are not public, and they rotate among factors rather than allocate to different factors. So, indulging in a bit of factor timing. It is a good one to track and when we have more data, we can do a simple regression to figure out how much loading of each factor is being delivered by the fund.

Until then it’s a fantastic opportunity for DIY investors or boutique fund managers, in India, who would like to follow a rules-based strategy. They can study the methodology used to create these indexes and create their own portfolios based on the rules used to create these indexes. They can also use products like smallcase which have many of these factors pre-packaged in portfolios made in-house as well as by other investment advisors.

Berkshire Hathaway’s 1994 annual report

If you want to beat almost 90% of professional money managers and get market returns along the way, just buy the simple low-cost market cap-weighted index fund as your main course and to attempt to outperform add some active funds and other beta strategies for dessert.

Beta is beta. Smart Beta is just another name for a factor as defined earlier. It’s not smart or dumb. Market beta has different characteristics from momentum, low vol, size and value as they do from each other. What is important is that they should be defined simply, be packaged in a low-cost vehicle and deliver results over time in a robust manner. Rest is marketing to keep your monkey brain happy.

Clifford Asness, who manages over $180 bn in quantitatively driven strategies and someone who did his Ph.D. under Gene Fama, says “Market cap-based indexing will never be driven from its deserved perch of as core and deserved king of the investment world. It is what we should all own in theory and it has delivered low cost, equity returns to a great mass of investors….the now and forever of king-of-the-hill.” And if you are not a full-time investor, that is where the majority and “core” of your portfolio should reside.

Further Reading

1. Your Guide to Factor-Based Investing by Andrew L. Berkin and Larry E. Swedroe

2. Quantitative Momentum by Wesley R. Gray and Jack R. Vogel

3. Quantitative Value by Wesley R. Gray and Tobias E. Carlisle

4. The Little Book That Still Beats The Market by Joel Greenblatt

5. Buffett’s Alpha (2013) by Andrea Frazzini, David G. Kabiller, and Lasse H. Pedersen

6. AQR Research

7. A Conversation with NYU Professor Aswath Damodaran - views on indexing, market efficiency, factor investing and why investors ignore momentum at their peril.

🙏 Thank you for reading through my rant. You can keep the conversation going on the Indexheads Facebook group.

The goal of Indexheads is to spread the virtues of low-cost investing. We publish this newsletter just to create awareness about the merits of index funds. If you liked reading this issue, do you think it’s worth sharing? If yes, click 👇 the share button.