The Indexheads India newsletter

Dedicated to spread the word about low-cost investing.

Hello folks and welcome to Indexheads,

Today, your chances of picking a fund that can consistently outperform the index is worse than a coin toss. Given the new reality, the logical thing for you to do is to invest in low-cost index funds. But not many people know the importance of costs, let alone index funds. Indian mutual fund investors still believe that regular mutual funds are free.

I was thinking of a way to spread the word about the virtues of low-cost index investing among both investors and among the advisor community. Posted a Tweet soliciting views:

Anish offered help to make this a reality and lo and behold.

The goal of this newsletter is to spread the gospel of low-cost disciplined investing. For us, it’s not about active vs. passive, but rather low-cost vs. high-cost. Active isn’t bad, but active management at a high-cost is BAD!

Each fortnight, we’ll bring you the best perspectives both ours as well as curated gyaan from across the finternet (financial internet).

I am an investor first and foremost, and I had my passive awakening recently. And with this newsletter I want to scream as loudly as possible, about the importance of costs and not doing, dumb shit for as many investors to hear as possible.

I don’t have a new fund nor an options strategy to sell :)

Who are we?

Passivefool

I am an anonymous idiot on Twitter. As the name implies, I am a fool and a lifelong learner. But the one unfoolish thing I do correctly is investing in low-cost index funds. So, here to spread the word about the one right thing I do in life :)

I run QED Capital – A boutique PMS firm based in Mumbai. I am passionate about simplifying investing for all and indexing. Stems from my personal experiences as a child (my father was a successful doctor but knew nothing about saving and finances). So when Passive Fool put out the tweet above, I joined him to pitch in. We also have a Facebook group which I would urge you all to join and be a part of the Indexing journey.

Why indexing?

Wokay, strap yourselves in peoples, this is going to be a long rant.

Part 1 - The greatest trick

Scene 1 - Prelude

In the past 500-1000 years, there have been some monumental discoveries. Inventions such as the printing press, telescope, electricity, the telephone, the steam engine, computers, internet, incognito browsing, 3D porn (in that order 🤪), Instagram, selfie-sticks, dog nail polish, the baby mop, and so on.

These inventions have changed the course of humanity and also the pace of our hand movements 😜

If you ask someone to list some important inventions, you’ll pretty much hear the same names as above, except for the retarded ones I’ve mentioned. However, one thing you will never hear is the automatic deduction of fund management fees.

Just think about the beauty of this setup for a minute. Every year, fund managers and asset management firms make over Rs 17,000 crores in India alone, and billions globally in fund fees and every single penny is automatically deducted. The average investor won’t even know he is paying, let alone realize that he is paying high fees.

This reminds of this quote from the movie, The Usual Suspects:

The greatest trick the Devil ever pulled was convincing the world he didn’t exist.

This can, in the investing context, be paraphrased as:

The greatest trick the investment management industry pulled was to convince you into convincing yourself that you aren’t paying anything.

Imagine an alternate universe where you had to manually pay fund management fees every month by writing a cheque or through an online transfer. We hardly give a shit about fund fees now. But we sure as hell would if we had to pay month in month out.

There are thousands of variables that impact investment performance, but except for the fees and our behaviour, we cannot control the rest. But as is the tradition among retail investors, we screw up both of these. We don’t give a damn about the fees we pay and to compound the misery, we do dumb things like market timing, chasing investment fads, and taking investment advice from Twitter.

End of scene 1.

Scene 2 - Scented bullshit

The fund management industry is brilliant when it comes to marketing - AKA scented bullshit. They convinced us that:

Close-ended funds are good because the lock-in allows the fund manager to have a long-term view

L&T Emerging Opportunities Fund – Series II (a three-year close-ended fund) offers an upfront commission of 5% to distributors, Sundaram Multi-cap Fund – Series I NFO (new fund offer) (a five-year close-ended fund) offers 6.50%. - Livemint

That debt funds, especially FMPs, were better than FDs

Source: Manoj Nagpal

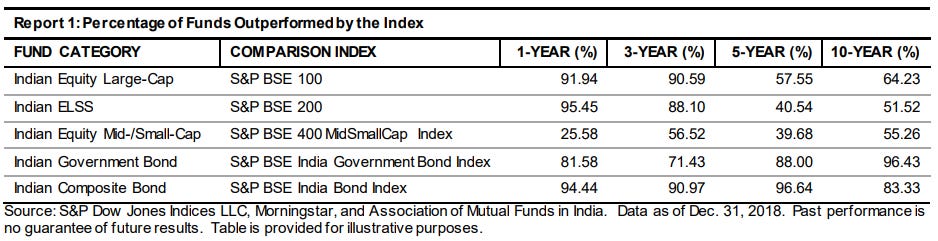

But perhaps, the greatest trick they pulled is convincing investors that they can beat benchmarks or deliver “alpha.”

Source: SPIVA India

But most of the retail investing crowd is uninformed and chooses to remain stubbornly dumb. Moreover, given their Jupiter sized egos, they refuse to see this.

Still reading? Feel like hitting me with a slipper? Good! Read on a little more.

Ok, so you’ve said that mutual funds are bad, most fund managers are liars, and retail investors are egoistic dumbasses. What the hell?

Wokay, here’s where the plot takes a twist!

In 1975, an unknown gentleman by the name John Bogle (Jack Bogle) started a firm called Vanguard. In 1976, he launched the world’s first index fund - The Vanguard 500 Index Fund. I don’t think Jack had realized at that point, that this simple act would lead to nothing short of a revolution and the collective betterment of millions of investors worldwide. He basically told the Wall Street fat cats to go screw themselves, in his own way.

When Jack launched the Vanguard 500 Index fund, the industry derisively labeled the fund as “Bogle’s folly.” From one of Jack’s speeches:

But there remained a multitude of strident critics of indexing. They were well described by Rex Sinquefield of American National Bank, an early advocate of the concept. Writing in Pensions & Investments he said: "As talk of market (i.e., index) funds moves from the discussion of debate, the exchange is often enlivened but seldom enlightened. Critics of these funds have suggested that market funds are a 'cop-out' and a search for mediocrity. Some have said they are downright un-American. Few, if any, investment concepts have been the object of so much scornful ridicule. The vitriol and paranoia permeating so much of the criticism reveals a profound misconception of the role that market funds should play in institutional portfolios."

When Sinquefield wrote those words in 1975, we had not yet filed our fund—designed for individual investors—and when we did, in mid-1976, the criticism was hardly muted. It was described as "Bogle's folly" more than once. Fidelity Chairman Edward C. Johnson III doubted Fidelity would soon follow Vanguard's lead. "I can't believe," he told the press, "that the great mass of investors are [sic] going to be satisfied with just receiving average returns. The name of the game is to be the best."

Bogle’s folly!

Vanguard, right from its inception, has been all about low costs. Jack Bogle and Vanguard by extension, brought down fund fees to bargain-basement levels and dragged the entire US asset management industry along, which was content with happily ripping of the average investors along. Just look at the graph above! Anyway, we’ll talk about the history of index funds in subsequent issues. Back to the issue hand.

An average investor’s journey typically starts along these lines. Hoping to make a quick buck, he starts as an intraday trader, then becomes a positional trader because the stock falls and becomes a long term investors because the stock be bought was RCOM 😂. But, on a serious note, the average investor’s journey goes something like this:

Every lay investor dreams of picking the next Infosys or the next HDFC, so do I. But the odds of that are Infinitesimally low. Let me put that into perspective. Hedge fund managers and mutual fund managers have all the information on the planet. They have million-dollar research budgets, flocks of analysts, and a parade of PHDs and other smartasses. They use artificial intelligence, machine learning, and even fricking satellites and drones. All this to beat the market? You’d be excused for thinking that they would have succeeded given this edge. Wrongg!!! They suck!

They have been unable to beat a simple Nifty 50 index fund.

US hedge fund managers have been unable to beat a simple S&P 500 index fund

I’ll let Charles Ellis do the talking as to why trying to beat the market is a futile endeavour.

Ok, you’ve scared me shitless. Do I even invest or put my money in fixed deposits.

Things aren’t that dire :) Look, the point I wanted to make is that your chances of beating the market or picking a stock or a manager than can outperform the market consistently are worse than a coin toss. Today, the best thing you as an investor can do is to invest in index funds. But the problem in India is that we don't have too many choices when it comes to index funds given that our markets aren’t liquid.

We have large-cap index funds but, we don’t yet have any index funds that track mid and small-cap indices. Understandable, given that liquidity dries up pretty quickly outside the top 200 odd stocks. Mid and small-caps become even more illiquid during the market phases like the one we are going through.

Today, it’s a no brainer to have index funds as your core allocation. You can continue to invest in good active mid and small-cap funds with consistent track records who stick to their mandates until we have mid and small-cap index funds. And if you still have the itch to do things like trade or chase the next hot stock, theme or sector, put a small sum of money you can afford to lose and not cry about in a separate account and go bananas.

Oh my god, enough with your sanctimonious BULLSHIT! Just tell me why this newsletter and now?!

Indian investors don’t seem to know the importance of costs and or they seem to be oblivious if they do. In 2013, SEBI mandated that fund houses off direct plans of all mutual funds with 0 commissions. Today, nearly 5 years later, only 16% of the AUM is in direct plans. We don’t have a break of the retail vs. institutional AUM but fee-only financial planner Avinash Luthria put this number at 5%.

Index funds have been around for a while now and yet, just about 4% of the 25 lakhs crores of the total AUM is in index funds. Again, the lion’s share of this is Employees’ Provident Fund Organization (EPFO) money.

And Scene!

Do subscribe to stay updated and help us spread the word about the benefits of low-cost index investing. Also join our Facebook group for interesting discussions on all things indexing and investing :)