Apparently, it's too early for the active vs passive conversation in India

Issue #18

Not a day goes by when I don't hear some utterly silly attack against the humble index fund. I've said this again, and I'll say it again, there are very few things in the world of finance that have done as much as the humble index fund has done to create positive financial outcomes for common people. Tim Hartford rightly even included the humble index fund in his podcast series 50 Things That Made the Modern Economy. The invention of the index fund has been an unmitigated good that has democratised low-cost access equities to the India growth story (I know I make fund of this phrase) for every Indian.

But the salespeople don't like the index funds, and they wish it was never created. And how does the asset management industry react to the index fund that is eating into their fat juicy margins? By creating duplicitous narratives and false equivalencies. To paraphrase Jim Cramer, "every once in a while, you hear something so stupid it takes your breath away." And this is an issue where I talk about one such narrative.

It's also often necessary to repeatedly explain what an index fund is and what it promises because to quote Rick Ferri, "the truth about index investing must be told over and over again because lies are constantly being told around it."

A plain vanilla broad market index fund gives you low-cost exposure to a broad slice of the market—end of the story, no ifs and no buts. There are no fancy methodologies, black boxes, complicated structures etc. If you invest in a Nifty 50 index fund, all you are getting is exposure to the 50 biggest companies in India by market cap in the same proportion as the index, and you'll get the same returns minus costs as the Nifty 50 index - THE END! Why do people hate on this humble little fund, goddamn it?

A lot of myths are perpetuated by people whose livelihoods depend on selling costly funds that subtract value from investors. I'll spend the next few issues debunking these myths that are designed to mislead investors.

One of the oldest and perhaps the most deceptive narratives about the humble little index fund in India is that it is too early to talk about index funds. I had heard this narrative from the AMCs multiple times, and I didn't think much of it. The reason being, at some level I understood that pretty much all of the Indian AMCs are traditional active giants and they have got to make a living. It's not like they can wake up one fine morning, read the gospel of John Bogle, shut most of the closet index funds and launch actual index funds. It's not right what most AMCs are saying about index funds, but I understand how difficult it is to run an asset management firm.

But what set off the alarm bells this time for me was this narrative, this myth about index funds got an upgrade. It's not only too early to discuss active vs passive in India, but apparently, this discussion was confusing investors, and the focus should apparently be on getting them to invest first rather than confusing them with terms like active, passive, benchmarks etc.

Just pause here for a second and read what I said again, and you'll appreciate the sheer brilliance of this narrative. It's stupid, but it's so brilliantly crafted, it can almost trick you into believing that it is true. I want to unpack these two parts separately.

Is too early for the active vs indexing (passive) debate in India?

Saying it's too early to talk about indexing is like saying it's too early to talk about just eating vs eating healthy. Why focus on nutrition, dietary dos and don'ts, etc.? Why not tell people just to eat whatever garbage they can find? Why worry about healthy diets? After all the goal is not to be hungry!

If you read this previous issue where we wrote about the story of the index fund, then you'll recognize the script. It was the exact same thing Jack Bogle went through. When Jack launched the first index fund, all the Wall Street giants, including the likes of Fidelity, launched brutal and relentless attacks against the first index fund he launched. Quoting from the previous issue:

Edward Johnson, the Chairman of the Fidelity Group, one of the biggest asset managers even at that time, said:

“I can’t believe that the great mass of investors are [sic] going to be satisfied with just receiving average returns. The name of the game is to be the best.”

Competitors:

“Who wants to be operated on by an average surgeon?”

We are going on record now because of the wave of publicity about index funds that, by their charter need to do no better than the average. As professionals, we reject the thought of settling or the averages. Whatever road other fund managers take we are going to strive for excellence.

But we all know how the story turned out. Most of those active fund investors would've been better off just putting their money in an S&P 500 index fund.

But one of the insinuations of the AMCs when they say, “it's too early to talk about indexing in India” is that they are delivering outperformance by the boatloads since the dawn of time justifying the high fees. If you go by the popular narrative, the people who don't like index funds would have you believe that India is a land of milk, honey and is overflowing with alpha everywhere. Not just overflowing, there apparently are waterfalls of alpha next to NSE and BSE buildings where managers regularly get some.

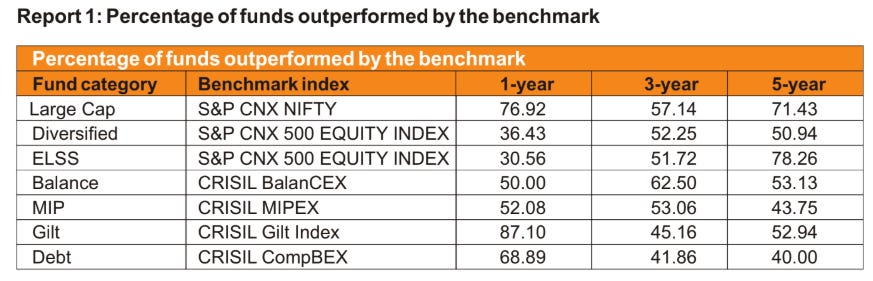

Shall we look at the numbers? Fortunately for us, SPIVA has been keeping track for the performance of active funds vs a broad benchmark for a long time.

Here are numbers from SPIVA 2010

Now, remember, these were the days when we had entry loads, and fund houses didn't have any restrictions on the number of funds they could run or how they manage them. A fund could be called large-cap and invest in mid and small-caps; there were no comprehensive categorization guidelines.

SPIVA 2012

SPIVA 2015

This is after the Modi bull run started.

It's abundantly clear that any given point of time 50-70% plus equity funds underperformed the index. Your odds of picking a consistent fund, at least in the large-cap space was always worse than a coin toss, a hit or a miss. There you go. Clearly, it is still very early to have the active vs passive debate in India. My god I started writing about index funds way too early 👇

👋Hello from the closet

Rajan Raju, Ananya Mittal, and Rajiv Baruah recently published a brilliant paper titled "Diversification within Large Cap Equity Mutual Funds in India". They looked at if there was any benefit to choosing an active large-cap fund vs an index and fund and look at the graph below. It shows the active share of large-cap funds.

Active Share measures how different the holdings of an active fund are from its benchmark index. So, if the active share is 50%, it means that 50% of the fund's holdings are identical to the index. Anything below 60% is usually considered closet indexing (benchmark hugging). I'll reach out to Ananya, Rajan and Rajiv and see if they would be open to maybe writing about the paper here on Indexheads. Would be so fricking awesome.

In the conclusion of the paper, the authors noted:

The cross-sectional holding data in June 2020 indicates that many funds have followed the latter approach. There is a crowding together of large-cap funds. Staying aligned to the benchmark seems to be a conscious choice. The analysis of historical monthly returns shows a high correlation and positive covariance amongst large-cap funds. The IR of these funds show that they do not outperform the reference ETF on a risk-adjusted basis.

Denying that a vast majority of active funds fail to beat index funds is like believing drinking bleach/Domex can cure COVID, the earth is flat, and that Donald Trump is the greatest US president since Abraham Lincoln

Talking about index funds is apparently confusing investors

Let me start again by asking why do people hate the humble index fund so much?

The second part of the narrative of "it's too early for the active vs indexing (passive) debate" is that the focus should be getting people to invest rather than confusing them with terms like active, passive, benchmarks, the importance of costs etc.

If these things are confusing the investors, then why even talk to them about mutual funds? Let's just get to invest in LIC Jeevan Dhara, Chit funds, or Emu Farms? After all, the goal is to get them to invest. And these instruments need no explaining, at all.

Ok, the sarcasm aside, let's think this through logically. If a newbie who has zero clue about investing enters the markets and he has two choices:

1. A low-cost Nifty 500 index fund.

2. 460 active equity and hybrid schemes

Which one do you think he'll choose? On the one hand, if he buys an index fund, all he is doing is buying all the 500 biggest companies in India. On the other hand, if he has to choose an active fund, he has to look at the so-called fund managers processes, philosophies, their track records, managerial changes, historical fund allocations, the PDFs, PPT's, webinars, and a bazillion other things and make a judgement. If you're still going to say, that's why they are getting that delicious little alpha, didn't I just show you the numbers 🤬?

Let me make this real simple. Low-cost index funds should always be the centre of your investing universe or your core allocation. This core will be working for you, no matter what. You can put small amounts of your money to dabble in all the other fancy stuff to generate that extra return over and above the index funds. That is if you want to.

Made this silly illustration to explain this:

So, if the AMCs were honest, they would be recommending investors to put most of their money in low-cost broad market index funds as their core allocation. But what they are doing instead is propagating nonsense that proponents of index funds are confusing investors. These are the same AMCs are launching multiple NFOs every month in the name of making things simple for investors and selling costly sub-par funds 🙄. Sometimes, I feel like leaving the planet.

Look, the AMCs always have something to the other to sell. If you listen to them, they would have you invest in 12 equity funds, 6 hybrid funds, 16 debt funds and 10 FOFs. But cut out the nonsense and the noise and look at this objectively.

Why do Index funds work?

If you are reading this newsletter for the first time and are new to index funds, then you might probably be thinking index funds won't work because they're so easy to pick and there's no real skill or effort involved in picking. It's a fair thought. But as Morgan Housel says, the stock market is the only place where effort and results are not correlated. Just because active managers, put in all the hard work doesn't mean they're owed a return.

Over the past decade or so, the markets have become increasingly professionalized. Informational asymmetries or informational advantages that existed a decade ago are slim today. Everybody has the same information, the same Bloomberg terminals and they are all competing with each other. For every active manager with a big research budget, there are 10 more professionals with even bigger research budgets, army of PhDs, drones, satellites and other resources. And don't even by accident think that you can beat the market consistently, there are far bigger sharks in the water.

And then there are active managers who don’t want to upset the apple cart and stick close to the index while claiming they are active funds. Why, you ask? 80%+ of the Indian MF AUM is regular mutual funds, which means it’s from distributors. While there are shady distributors like the banks who just care about high commissions, there are some really good distributors who do actual advisory. Now, these advisors when they sell something to investors they’d like some certainty. They don’t want the manager in the fund they sold to be a cowboy and shoot from the hip. Worst case, they’d like their fund to resemble the benchmark. And to cater to these distributors, AMCs have arrived at a form of active management that is index + or - 2-5% to deliver index-like returns always. Not all active managers but most of them.

That doesn't mean you shouldn't try to outperform the market. But if you do want to, try with a small chunk of your portfolio and figure out if you're cut out for it.

But anyway, coming back to the point about what makes index funds work. One thing the advocates of low-cost indexing, including me, are guilty of is making the case for index funds all about the performance vs active funds, and this has always bugged me. This is mostly because the salespeople peddling sub-par active funds always use deceptive numbers, and we respond with data.

Of course, index funds outperform most actively managed funds. But I've always felt uneasy when talking about index funds from a returns point of view. Indexing works first and foremost because of its cost advantage:

The reason why index funds perform well over the long run is because of their cost advantage. The average expense ratio of the regular plans of large-cap active mutual funds is 2.25% while it’s 1.29% for direct plans. It’s 0.46% for regular plans of index funds and 0.30% for direct plans. So, an active fund has to generate a 1.29% (direct) extra return just to meet the benchmark and then generate additional returns over that to beat the benchmark - easier said than done.

It's always about the costs; they are the biggest drag on performance. Index funds have low-costs and add to the fact that there is minimal churn, unlike active funds which have a lot of turnover, index funds always have the edge.

Active or passive?

While we constantly show how terrible most active funds in India are, by no means am I saying you should put 100% of your money in index funds, that’s up to you to figure out. I know investors who don’t want to take part in the rat race of picking star managers. They don’t care about beating arbitrary benchmarks, and they consider their benchmark as to whether they reach a goal or not and just invest only in index funds and don’t bother with anything else.

Then there are investors who put a bulk of their money on index funds, say Rs 70-80 out of every Rs 100 they invest in equtites and the remaining in active funds. Some prefer to generate that outperformance with traditional discretionary active funds. And then some don’t trust human managers at all and instead choose to bet on factor, quant, or smart beta funds and ETFs because they are rules-based and they know what they are getting.

But the questions remains, how do you pick an active fund? People look at how consistent they are over a market cycle, look at how they capture the upside, and the downside, look at whether they stick to their stated mandate or not, various ratios and 100 other things. Some people bet on star fund managers. I made the same mistake when I was starting, and I picked an active manager because I had spoken to him and liked how transparent and honest they were. It was a really stupid way to pick a fund, but I didn’t know anything. And in a happy accident, it worked out really well for me.

But on the flip side, if I had chosen another star manager like Naren or Prashant Jain instead of the manager I picked, I would have underperformed a savings bank account for the last 5 odd years. Of course, it's debatable if 5 years is enough to judge a manager, but it would have been tough to stomach that when other managers and index funds were beating these managers black and blue.

To answer the question, not all active is bad. But picking the right kind of active is incredibly hard and which is why I prefer smart beta ETFs (not a recommendation). But even in smart beta funds, you need to remember that these funds are cyclical and can go a long time underperforming index funds. For example, Value has underperformed growth for nearly a decade in the US now. Diversification within factors also is an important factor each investor needs to consider before investing in factor funds (smart beta).

Know what you are getting into.

I am pretty sure some lazy investor will go pick a smart beta ETF just because it is written here on the newsletter without realizing their risks and just looking at past performance. I beg you to not do that.

A wise man once told me this which sums up investing for retail investors brutally and it’s called the Kangana complex:

There are the Kangana's of Indian FinTwit and then there are the Rakhi Sawants - (Rakhi Sawant's has huge loading on her actual carpet area but the super built up is not real.) So there are the Kangana's who have done well and have been successful in markets - whether by luck or skill or both - and now say only I can save you. I will fight the good fight against these passive buggers who say settle for average. And then there are Rakhi Sawants - who are forever posting screen shots of new backtests and strategy - are unable to replicate them in real time. They use them as hooks to land themselves training workshops and seminars where they will show you how they "did it".

Those workshops are like Kohli scoring a century off Anushka's bowling in their practice sessions during lockdown. It wont actually help Kohli score a century during IPL. We didnt say it - Gavaskar did. In jest though, he was misquoted and that is not what he meant. He didnt mean to undermine the bowling skills of an A-grade actor who has played a female wrestler and defeated no less than Salman Khan on screen. But coming back - these training and workshops (most of them - not all) are like that. These look good like Anushka and you get attracted thinking you are Virat Kohli.

So no surprises when you actually start trading on monday, you capital gets wiped out faster than RCB's score is chased by other teams

Wondering what you think about something like this: https://www.thehindubusinessline.com/opinion/columns/aarati-krishnan/why-india-needs-a-vanguard/article25519294.ece

Hi - I happened upon your blog after a friend forwarded me your tweet on the daylight robbery of HDFCs massive actively managed cash machines that consistently underperform the market. I totally subscribe to the same view on passive vs active. I worked in fin services in New York for 5 years (index trading, ETF market making, equity trading) before moving back to India last year, and couldn't believe the proliferation of these funds vs under penetration of passive ones (and ETFs!). I'd love to chat more about indexing and the passive world, and maybe even write/collaborate. I subscribed to you newsletters, but don't see any way to actually reach out to you directly, so have dropped this comment here - Jaisal